How Data-Driven Investment Theses Are Changing Venture Capital

Most investment theses live in an investor's head, which means they cannot scale, cannot transfer, and cannot be acted on systematically. Here is how the shift to explicit, data-driven theses is changing both sides of the early-stage funding table.

AngelHive

AngelHive

For most of venture capital's history, the investment thesis lived inside the investor's head. It was a set of intuitions about what kinds of companies tended to succeed, what characteristics a founding team needed, which markets were about to move. It was refined over years of pattern matching, right calls and wrong ones, and conversations with other investors who had done the same.

That model still exists, and it still produces good investors. But it has a problem that becomes more visible as deal flow grows: it does not scale, and it does not transfer.

When an investment thesis is implicit, it cannot be communicated clearly to a startup before they apply. It cannot be used to filter hundreds of applications automatically. It cannot be compared against portfolio outcomes to identify which elements actually predicted success. And when the investor moves on, or the fund scales up and hires analysts, the thesis is notoriously difficult to transmit.

The Shift Toward Explicit Theses

Something has been changing in how the most sophisticated early-stage investors operate. The shift is from intuitive, implicit thesis to structured, explicit thesis, and it is being accelerated by two things: the sheer volume of deal flow that modern investor communities face, and the availability of tools that can act on structured investment criteria at scale.

The number of data-driven VC firms jumped 20% from 2023 to 2024, demonstrating rapid adoption of AI-powered tools across the industry.¹ More than 75% of venture capital deal reviews are expected to incorporate AI and data analytics by 2025.² This is not about replacing human judgment. It is about creating the conditions under which human judgment can be applied to decisions that actually require it, rather than to initial screening of companies that were never going to be a fit.

A 2025 Bain and Company Global Private Equity report found that one fund reduced initial screening time from 45 minutes to 8 minutes per company using automated scoring, allowing partners to evaluate more than 200 additional companies monthly.³ That is not a productivity gain at the margins. It is a fundamental change in how many opportunities a fund can see and evaluate in a given period.

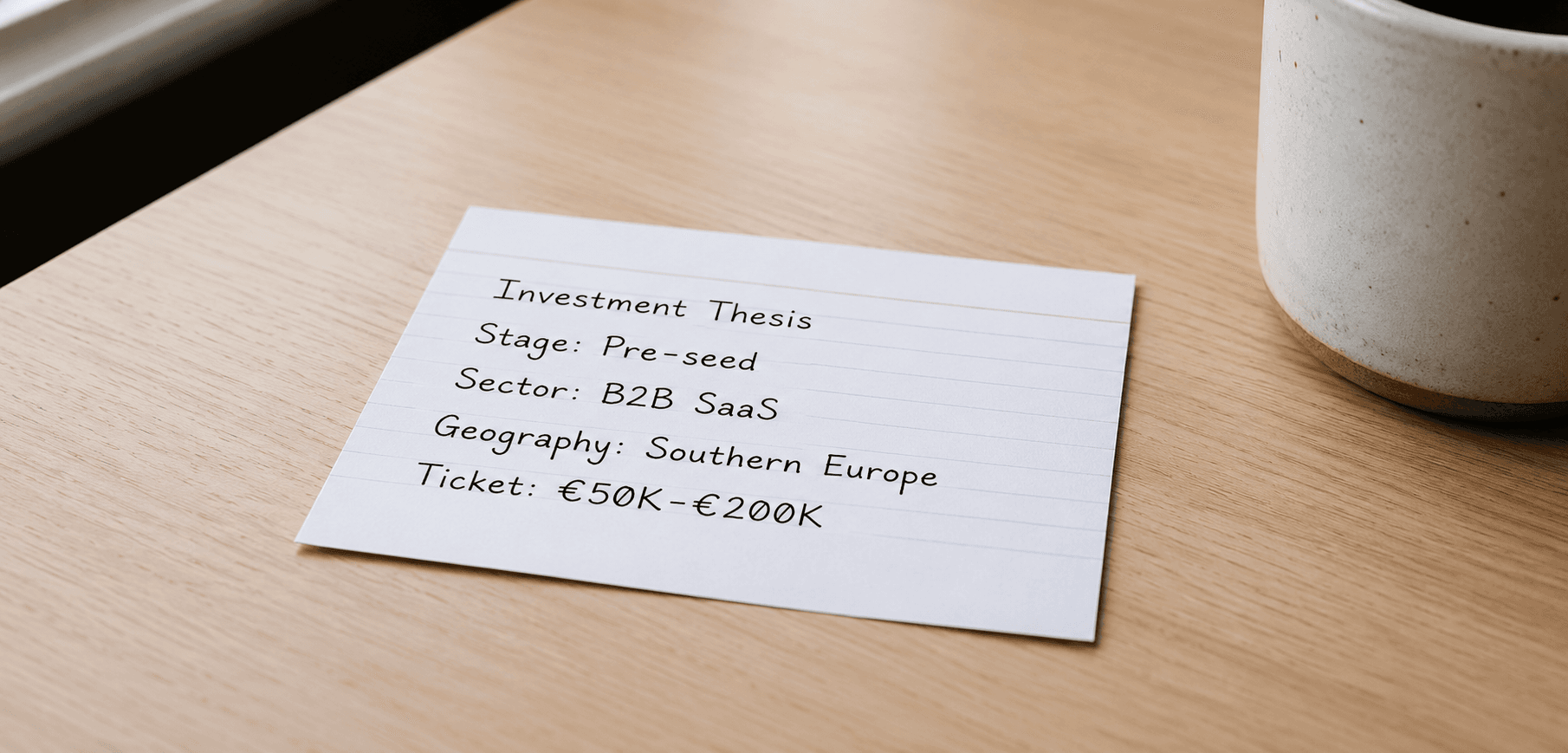

What an Explicit Thesis Actually Looks Like

An implicit thesis might be: we like B2B SaaS companies with strong founding teams in markets we understand.

An explicit thesis looks different. It specifies stage, sector, geography, ticket size, and team criteria. It also specifies what the investor does not want: companies with no revenue traction after 18 months of operation, founding teams with no relevant industry experience, or markets where regulatory approval is the primary path to revenue.

When a thesis is written down at this level of specificity, several things become possible that were not possible before. Applications can be filtered automatically against it. Startups can check their own fit before applying, saving time on both sides. And over time, the thesis can be compared against actual outcomes to see which criteria were actually predictive.

The Problem with Gut Feeling at Scale

The intuitive model of deal evaluation has a structural weakness that rarely gets discussed openly: it is inconsistent. The same company, evaluated by the same investor at different times or in different emotional states, can receive different assessments. An investor who sees a strong deal early in the day may evaluate the next deal more harshly by comparison.

This is not a character flaw. It is a feature of human cognition. But it produces investment decisions that have more noise in them than most investors would be comfortable acknowledging.

Structured evaluation does not eliminate this. But it introduces a layer of consistency that acts as a counterweight. When every application is assessed against the same framework, the signal-to-noise ratio improves. Companies that would have been overlooked because they were submitted at the wrong moment, or because their deck was rougher than a competitor's despite stronger fundamentals, have a better chance of surfacing.

What This Means for Startups

The shift toward explicit theses changes the experience of fundraising for founders in ways that most have not yet fully registered.

The most significant change is relevance. When an investor has a well-defined, public thesis, a founder can evaluate fit before investing the time in an application. Most investor mandates are vague on their websites, communicated imprecisely in conversations, or simply not communicated at all. Founders apply broadly because they cannot easily determine who is actually likely to say yes.

When thesis definitions become structured and machine-readable, that changes. A platform that holds the investment criteria of dozens of investor communities can match a startup's profile against all of them simultaneously. That shifts the fundraising process from lottery to something closer to a targeted search.

The second change is feedback quality. An AI assessment of a startup's application, generated against a specific investor's thesis, tells the founder something meaningful: here is where you are strong relative to what this investor cares about, and here is where there is a gap. Even when the outcome is a pass, that is more useful than silence.

The Limits of the Data-Driven Approach

It is worth being honest about what structured, data-driven investment processes cannot do.

They cannot evaluate founder resilience with any reliability. They cannot predict whether a market that looks unattractive today will shift in three years. They cannot assess the quality of interpersonal dynamics within a founding team, or whether the founder's understanding of their customer is genuinely deep or just plausible-sounding.

These are judgment calls that require human involvement. The value of a data-driven approach is not that it replaces those judgment calls but that it concentrates them. An investor who spends less time screening clearly mismatched applications has more time and cognitive capacity to apply genuine judgment to the companies that deserve it.

The best investment processes combine explicit thesis definition with AI-assisted initial evaluation, and reserve the deeper qualitative judgment for the companies that have already passed through the first filter. That is a division of labor. The systematic parts handle volume. The human parts handle judgment. Neither works as well without the other.

---

AngelHive connects startups with investors who have defined their thesis explicitly, so every match is based on genuine fit rather than chance. Apply or join as an investor community at angelhive.io

---

1. Data Driven VC Landscape 2025, cited in multiple industry sources including syndicateroom.com/articles

2. Multiple industry reports including Alpha Hub, "AI-Driven Due Diligence: How Artificial Intelligence Is Transforming Venture Capital," January 2026, alpha-hub.ai/blog

3. Fifty One Degrees, "How Venture Capital Firms Are Using AI and Data Science to Transform Investment Strategy in 2026," citing Bain & Company Global Private Equity Report 2025, 51d.co/how-venture-capital-firms-are-using-ai/